The Certificate of Deposit (CD) Calculator can help determine the accumulated interest earnings on CDs over time. It also takes into consideration taxes to provide more accurate results.

Certificate of Deposit (CD) Calculator

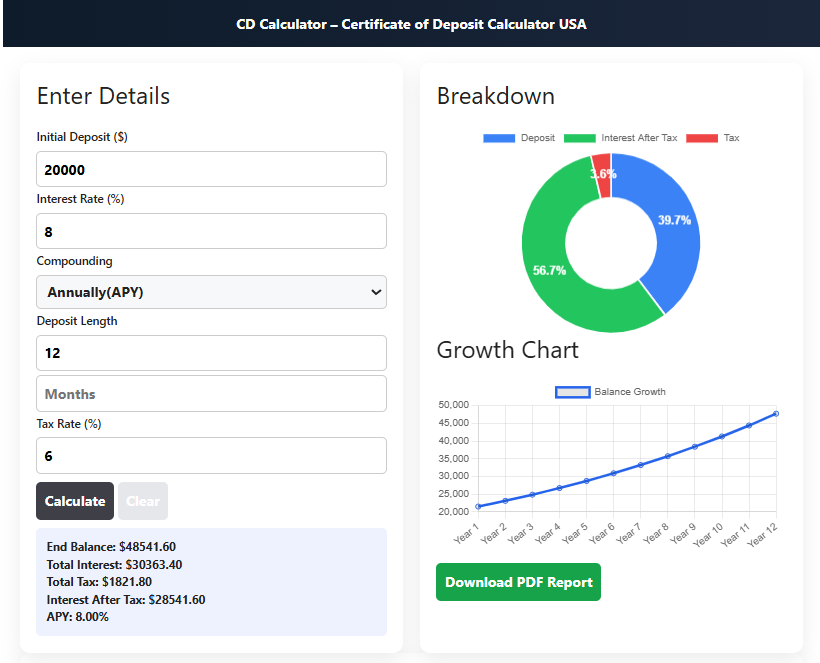

Calculate your CD maturity value, total interest earned, APY, after-tax returns, and view full amortisation schedules. Supports all compounding frequencies.

What is a Certificate of Deposit (CD) Calculator?

A Certificate of Deposit (CD) Calculator is a free financial tool that helps you determine exactly how much your deposit will grow over a specific period at a given interest rate and compounding frequency. By entering your initial deposit, interest rate, term length, and compounding frequency, you instantly receive your projected end balance, total interest earned, Annual Percentage Yield (APY), and after-tax returns — all without any manual calculations.

Our MyToolCalculator.com CD Calculator goes further by generating a complete amortisation schedule showing monthly and annual breakdowns, canvas-based visual charts illustrating your deposit growth, tax impact analysis, and a downloadable PDF report — making it one of the most comprehensive free CD calculators available online.

How CD Interest Works

A Certificate of Deposit is a savings product offered by banks and credit unions. Unlike a regular savings account, a CD requires you to lock in a fixed deposit for a set period — the term — in exchange for a fixed, typically higher interest rate. During this term, your money earns interest, which compounds based on the frequency your bank specifies.

The Compound Interest Formula

The fundamental formula powering CD calculations is:

A = P × (1 + r/n)^(n×t)

- A = End balance (maturity value)

- P = Principal (initial deposit)

- r = Annual interest rate (decimal form)

- n = Compounding frequency per year

- t = Time in years

For example: $10,000 at 5% compounded monthly for 2 years: A = 10,000 × (1 + 0.05/12)^(12×2) = $11,049.41

APY vs Interest Rate — What's the Difference?

The Annual Percentage Yield (APY) and the stated interest rate (APR) are related but different. The APY accounts for the effect of compounding — how frequently your interest is added to your balance — whereas the APR is simply the stated annual rate without compounding.

APY formula: APY = (1 + r/n)^n − 1

| Compounding Frequency | 5% APR Results In APY Of |

|---|---|

| Annual | 5.000% |

| Semi-Annual | 5.063% |

| Quarterly | 5.094% |

| Monthly | 5.116% |

| Daily | 5.127% |

More frequent compounding means a higher APY and more money earned. Daily compounding is the most beneficial for savers.

Tax Considerations on CD Interest

CD interest is considered ordinary income by the IRS in the United States and is taxed at your marginal federal income tax rate, plus any applicable state taxes. This means the true return on your CD is lower than the gross interest rate suggests. Our calculator includes a tax rate input so you can see your real after-tax earnings clearly.

Important tax notes for CD investors:

- Interest is taxable in the year it is earned, even if you don't withdraw it

- Your bank will issue a Form 1099-INT for interest of $10 or more

- CDs held in IRAs or 401(k)s are tax-deferred or tax-free, potentially dramatically improving returns

- Combined federal + state tax rates typically range from 20%–40% depending on your income bracket and state

Benefits of CDs

- FDIC/NCUA Insured: CDs at banks and credit unions are federally insured up to $250,000 per institution — zero risk of loss

- Higher Rates: CDs consistently offer higher interest rates than standard savings accounts

- Predictable Returns: Fixed rate for the full term means no surprises — you know exactly what you'll earn

- Variety of Terms: CDs range from 3 months to 5+ years, allowing flexible planning

- Low Minimum Deposits: Many banks offer CDs starting at $500–$1,000

- Disciplined Saving: The locked-in nature discourages impulse spending

Risks and Limitations of CDs

- Early Withdrawal Penalty: Withdrawing before maturity typically forfeits 3–12 months of interest

- Inflation Risk: If inflation exceeds your CD rate, your real purchasing power decreases

- Opportunity Cost: Money in a CD can't be invested in higher-return assets during the term

- Interest Rate Risk: If rates rise significantly after you lock in, you miss out on better returns

- Liquidity: Funds are not accessible during the term without penalty

CD Laddering Strategy

A popular strategy called CD laddering involves splitting your total investment across multiple CDs with different maturity dates (e.g., 1-year, 2-year, 3-year, 4-year, 5-year). As each CD matures, you reinvest at current rates. This balances higher long-term rates with regular access to funds, reducing both interest rate risk and liquidity risk simultaneously.

CD Calculator – Estimate Your Savings with Best CD Rates

What is a Certificate of Deposit?

Looking for a reliable CD calculator to estimate your savings? You’re in the right place.

A CD calculator is a financial tool designed to estimate how much your investment will grow over time.

It calculates:

Final maturity amount

Total interest earned

Tax on CD earnings (USA)

Growth with monthly or annual compounding

Using a certificate of deposit calculator USA, you can clearly understand your earnings before investing your money.

A Certificate of Deposit (CD) is one of the safest ways to grow your money in the United States. But here’s the reality — most people don’t know how much they will actually earn.

That’s where this CD calculator monthly compounding tool comes in. It helps you quickly calculate your returns using the best CD rates available, so you can make smarter financial decisions without guesswork.

How to Use This CD Calculator :-

Using this CD calculator monthly compounding tool is simple and fast:

- Enter your initial deposit

- Add your interest rate (APR)

- Select compounding frequency

- Enter your deposit duration (years and months)

- Add your tax rate (USA)

- Click on calculate

Within seconds, you will see your total earnings, interest, tax, and final balance with Breakdown and Growth Chart in the Visual Format.

Why This CD Calculator is Important

Here’s the deal — not all CDs offer the same returns.

Even if two banks offer similar interest rates:

- Compounding frequency can change earnings

- Taxes reduce your actual profit

- Duration affects total growth

That’s why using a CD calculator is essential before choosing the best CD rates.

Compounding Frequency and Understand Monthly Compounding

The calculator contains options for different compounding frequencies. With CD calculator monthly compounding, interest is added every month instead of once a year.

This leads to:

- Faster growth

- Higher returns

- Better APY (Annual Percentage Yield)

Over time, even small differences in compounding can significantly increase your earnings.

Real Life Example

Lets Assume:

Deposit: $10,000

Interest Rate: 5%

Term: 3 years

Compounding: Monthly

Tax Rate: 24%

Using this CD calculator, you can easily calculate:

- Total interest earned

- Tax paid on interest

- Final balance after tax

This helps you compare and choose the best CD rates in the USA.

Benefits of Using This CD Calculator

Instant and accurate results

Shows real earnings after tax

Helps compare best CD rates

Visual charts for easy understanding

Monthly and annual breakdown

Pro Tips for Better CD Returns

- Always compare APY instead of APR

- Choose CDs with monthly compounding

- Check tax impact before investing

- Avoid locking funds without planning

Types of CDs (Certificate of Deposit)

Understanding different types of CDs is important before using a CD calculator or comparing the best CD rates in the USA. Each type has its own benefits, risks, and flexibility.

1. Traditional CD

A traditional CD is the most common type of Certificate of Deposit.

- Offers a fixed interest rate for a specific time period

- Funds cannot be withdrawn before maturity without a penalty

- At maturity, you can withdraw money or roll it over into a new term

If the deposit is $100,000 or more, it is called a Jumbo CD, which usually offers higher interest rates.

2. Bump-Up CD

A bump-up CD allows you to take advantage of rising interest rates.

- You can increase your rate once or multiple times during the term

- Best for periods when interest rates are going up

However, these CDs usually start with lower rates compared to traditional CDs.

3. Liquid CD (No-Penalty CD)

A liquid CD offers flexibility to withdraw funds early.

- You can withdraw money without penalty

- Requires maintaining a minimum balance

- Interest rates are lower than other CDs, but still higher than regular savings accounts

Ideal for people who want both returns and liquidity.

4. Zero-Coupon CD

A zero-coupon CD works differently from standard CDs.

- Does not pay regular interest

- Purchased at a discounted price

- Full value is received at maturity

These CDs usually have longer terms and can carry higher risk, especially if interest rates change.

5. Callable CD

A callable CD gives the issuer (bank) more control.

- The bank can terminate the CD early after a certain period

- You receive your principal + earned interest

Because of this risk, callable CDs often offer higher interest rates compared to other CDs.

6. Brokered CD

A brokered CD is sold through brokerage firms instead of banks.

- Available via investment platforms

- Offers access to a wide variety of CDs

- Can provide better rates and options

Useful for investors who want to compare multiple CDs and find the best CD rates in the USA.